What is a Cash Flow Statement?

Cash Flow Statement

The cash flow statement is one of the most important reports a business can run. Like a balance sheet and profit and loss statement, the cash flow statement provides information on the health of your business and is frequently used by investors and financial institutions to assess profitability.

A cash flow statement is a budget summary that gives data about the changes in cash and cash equivalents of a business. The statement of cash flows acts as a bridge between the balance sheet and income statement by displaying how money moved in and out of the business.

The cash flow statement is believed to be the most intuitive of all the budget summaries since it follows the money made by the business in three primary ways—through operations, investment, and financing. The sum of these three segments is known as net cash flow.

A cash flow statement provides insight into changes in your cash on hand. This means that it covers three key aspects of your business activities. These are as follows:

- Operating Activities

- Investment Activities

- Financing Activities

This refers to regular business activities. Inflows include revenue from selling products or services, dividends received by the business, interest, and other cash receipts, Outflows include payroll, overheads, taxes, and payments to suppliers and vendors.

Cash Flow from Investing Activities includes the acquisition and disposal of non-current assets and other investments not included in cash equivalents. Investing activity includes the cash flows associated with buying or selling property, investing in fixed deposits, mutual funds, stock market, plant, and equipment (PP&E), other non-current assets, and other financial assets.

Cash Flow from Financing Activities result in changes in the size and composition of the equity capital or borrowings of the entity. This activity includes borrowing and repaying bank loans, and issuing and buying back shares. The payment of a dividend is also treated as a financing cash flow.

To properly prepare your cash flow statement, you need to have your income statement and balance sheet on hand. Below steps explains how to use a cash flow statement.

- Step 1: Calculate your Net Income

- Step 2: Convert your Net Income to Net Cash from Operating Activities

- Step 3: Calculate the net cash from net cash financing activities and investing activities

You can calculate your net income by referring to the income statement. Your operating activities are reflected in the income statement. Basically, your net income is a product of your gains and overall revenue, in a given time frame, minus your losses and total expenses, over the same time frame. However, your net income is not similar to your cash flow.

Your income statement is based off of the accrual method of accounting, and thus adjustments need to be made to pacify net income with net cash. With accrual method, you have a policy for recognizing revenue, this is often connected to doing the work or providing the service, and you record your expenses when a commitment is made, like when you agree to pay someone or sign a contract.

This means your income statement reflects losses or gains that might not actually be reflective of the cash you have on hand.

Once you calculate your net cash flow from operating activities, it gets much easier further. You need to calculate your net cash flow from investing activities and financing activities. Each of these categories require adding your inflows, and subtracting your outflows — no adjustments necessary!

Once you have a number for net cash flows from all three activities, next you need to sum up these three values together. This will provide you with your net increase (or decrease) in cash flows for the given period of time.

Below are the 5 advantages of Cash flow statement

- Verifying Profitability and Liquidity Positions

- Verifying Capital Cash Balance

- Cash Management

- Planning and Coordination

- Superiority over Accrual Basis of Accounting

Cash Flow Statement helps the management to ascertain the liquidity and profitability position of businesses. Liquidity refers to one’s ability to pay the obligation as soon as it becomes due. Since Cash Flow Statement presents the cash position of a firm at the time of making payment it directly helps to verify the liquidity position, the same is applicable for profitability.

Cash Flow Statement also helps to verify the capital cash balance of businesses. It is possible for businesses to verify the idle and/or excess and/or shortage of cash position, if capital cash balance is determined. After verifying the cash position, the management can invest the excess cash, if any, or borrow funds from outside sources accordingly to reach the cash loss.

If the Cash Flow Statement is properly prepared, it becomes easy for you to manage the cash. The management can prepare an estimate about the multiple inflows of cash and outflows of cash so that it becomes very helpful for them to make future plans.

Cash Flow Statement is planned on an estimated basis meant for the successive year. This helps the management to understand how much funds are needed and for what purposes, how much cash is generated from internal sources, how much cash can be procured from outside the business. It also helps to prepare cash budgets. Thus, the management can coordinate various activities and prepare plans with the help of this statement.

As a number of technical adjustments are made in the latter case, Cash Flow Statement is more reliable or dependable than collecting basis of accounting.

Cash flow can be calculated by 2 methods - Direct and indirect method.

- Direct Method

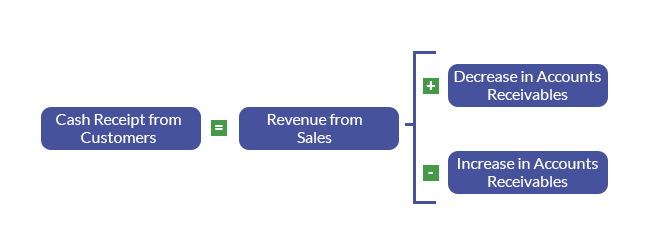

- Cash Receipt: Represents the actual amount of cash received during the period

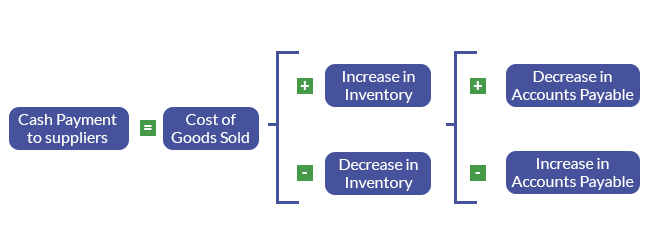

- Cash Payment: Represents the actual amount of cash payments to the suppliers

- Cash expenses may include selling, administration, R&D, and changes in other operating liabilities

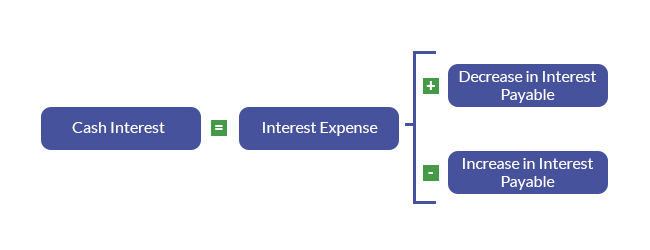

- Cash interest-only recognizes interest expense paid in cash

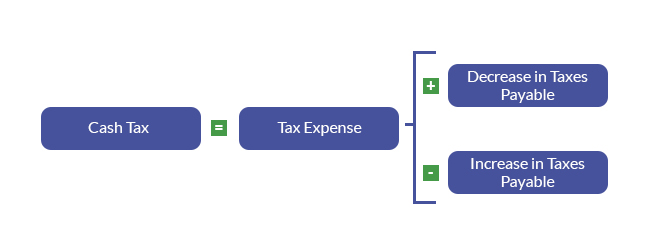

- Cash Tax: Represents only taxes paid in cash

The direct method uses actual cash inflows and outflows from the company's operations, instead of modifying the operating section from accrual accounting to a cash basis. Accrual accounting recognizes revenue when it is earned versus when the payment is received from a customer. This method measures only the cash that's been received, which is typically from customers and the cash payments or outflows, such as to suppliers. The inflows and outflows are netted to arrive at the cash flow. The direct method is also known as the income statement method.

Steps to calculate cash flow from operations using the direct method is given below –

Cash Flow (Direct Method) = Cash Receipts – Cash Payments – Cash Expenses – Cash Interest – Cash Taxes

Let us assume that ABC Business’s income statement sales was $650,000; gross profit of $350,000; selling and administrative costs of $140,000; and income taxes of $40,000. The selling and administrative expenses included $14,500 for depreciation.

Calculate Cash Flow from Operations using the Direct Method.

The following additional information is available

| Beginning of Period balance | End of Period balance | |

|---|---|---|

|

|

|

|

|

|

|

|

|

- Cash Receipt = $650,000 – ($81,000 – $65000) = $634,000

- Cash Payment = $300,000 – ($55,000 – $42,000) – (45,000 – $38,000) = $280,000

- Cash Expense = $140,000 – $14,500 = $125,500

- Cash Taxes = $40,000

Cash Flow from Operations using Direct Method formula = $634,000 – $320,000 – $125,500 – $40,000 = $188,500

The capital basis net income is established first in this method. This net income is then indirectly adjusted for items that affected the reported net income but did not involve cash. The indirect method adjusts net income for: changes in current assets , changes in current liabilities, and items that were included in net income but did not affect cash. Below are the detailed steps to calculate cash flow statement using indirect method:

Steps to calculate cash flow from operations using the indirect method is given below

- Start with Net Income

- Identify gains or losses that result from financing and investments (like gains from the sale of land).

- Identify non-cash charges to income and subtract all non-cash revenue components.

- Operating Assets: Increase in the balances of operating assets is subtracted while the decrease in those accounts is added

- Operating Liabilities: Increases in the balances of operating liability accounts are added, while decreases are subtracted

Cash Flow = Net Income + Gains & Losses from financing & investments + Non-cash charges + changes in operating accounts

Here’s an example of applying the indirect method :

Pam owns a chain of bakeries and is considering opening another storefront, but she wants to be sure her business is profitable enough to support such an investment. When looking at her year-end cash flow statements, Pam can use the following data:

- Net income: $200,000

- Depreciation: $20,000

- Accounts receivable adjustments: +$75,000

- Inventory adjustments: -$15,000

- Accounts payable adjustments: -$40,000

Let’s apply these data in the indirect method formula:

$200,000 – $75,000 + $15,000 – $40,000 + $20,000 = $120,000

Pam’s bakeries have an operating cash flow of $120,000, meaning she had $120k left over after all bills were paid. Depending on how much it has cost Pam to invest in new storefronts previously, she may or may not decide to use this leftover cash to pursue opening other retail locations.

- How is cash flow and net income differentiated?

- Why is cash flow necessary for business?

- How to maximize your cash flow?

- How to analyze cash flow?

- What happens when cash flow is negative?

- What is free cash flow?

- How to analyse if cash flow statements are correct?

- Can cash flow be negative?

- How to calculate Free Cash Flow (FCF) from a cash flow statement?

- What is levered free cash flow?

Cash flow is calculated by changes in cash balances from one accounting period to the next. Net income is gross income minus expenses in an accounting period.

Cash flow is important for businesses as it provides the money necessary to pay your bills, buy supplies, pay your employees, and keep your business operating.

To increase your cash flow, you need to start with speeding up the pace that your receivables come in. This may require reducing the time you bonus customers for paying on time or more customer service efforts.

To analyze cash flow you need to prepare a cash flow statement which will track how much money is coming in and out of your business. Then you can analyse your investments, operating expenses, financing costs etc.

Businesses cannot pay their bills when cash flow is negative. They’re forced to borrow money, pay interest, and hurt the bottom line.

Free Cash Flow (FCF) is the measure of money a business creates subsequent to considering capital consumptions.

In order to ensure that your cash flow statements are accurate, you’ll need to do a line by line analysis and verify that the information you input is accurate.

Yes, cash flow can be negative. It occurs when you have more expenses than income. It is the result of poorly managed receivables and the misunderstanding of how to use credit. For a limited time, negative cash flow is allowable, but repeated negative cash flow can cause a business to fail.

You can calculate FCF by taking your previous-tax and interest earnings, adding depreciation and amortization, and then subtracting changes in capital expenditures and working capital.

Levered free cash flow is basically money that is on deck after all debts are paid. It is money that is not owed to anyone. And, if you have stockholders or investors, it is available to them.